Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Protect Your Home With Homeowners Insurance

In addition to providing shelter and comfort, our home is often our single greatest asset, and it’s important that we protect that precious investment. Most homeowners realize the importance of homeowner’s insurance in safeguarding the value of a home. However, what they may not know is that about two-thirds of all homeowners are under-insured. According to a national survey, the average homeowner has enough insurance to rebuild only about 80% of his or her house.

What a standard homeowners policy covers

A standard homeowner’s insurance policy typically covers your home, your belongings, injury or property damage to others, and living expenses if you are unable to live in your home temporarily because of an insured disaster.

The policy likely pays to repair or rebuild your home if it is damaged or destroyed by disasters, such as fire or lightning. Your belongings, such as furniture and clothing, are also insured against these types of disasters, as well as theft. Some risks, such as flooding or acts of war, are routinely excluded from homeowner policies.

Other coverage in a standard homeowner’s policy typically includes the legal costs for injury or property damage that you or family members, including your pets, cause to other people. For example, if someone is injured on your property and decides to sue, the insurance would cover the cost of defending you in court and any damages you may have to pay. Policies also provide medical coverage in the event someone other than your family is injured in your home.

If your home is seriously damaged and needs to be rebuilt, a standard policy will usually cover hotel bills, restaurant meals and other living expenses incurred while you are temporarily relocated.

How much insurance do you need?

Homeowners should review their policy each year to make sure they have sufficient coverage for their home. The three questions to ask yourself are:

· Do I have enough insurance to protect my assets?

· Do I have enough insurance to rebuild my home?

· Do I have enough insurance to replace all my possessions?

Here’s some more information that will help you determine how much insurance is enough to meet your needs and ensure that your home will be sufficiently protected.

Protect your assets

Make sure you have enough liability insurance to protect your assets in case of a lawsuit due to injury or property damage. Most homeowner’s insurance policies provide a minimum of $100,000 worth of liability coverage. With the increasingly higher costs of litigation and monetary compensation, many homeowners now purchase $300,000 or more in liability protection. If that sounds like a lot, consider that the average dog bite claim is about $20,000. Talk with your insurance agent about the best coverage for your situation.

Rebuild your home

You need enough insurance to finance the cost of rebuilding your home at current construction costs, which vary by area. Don’t confuse the amount of coverage you need with the market value of your home. You’re not insuring the land your home is built on, which makes up a significant portion of the overall value of your property. In pricey markets such as San Francisco, land costs account for over 75 percent of a home’s value.

The average policy is designed to cover the cost of rebuilding your home using today’s standard building materials and techniques. If you have an unusual, historical or custom-built home, you may want to contact a specialty insurer to ensure that you have sufficient coverage to replicate any special architectural elements. Those with older homes should consider additions to the policy that pay the cost of rebuilding their home to meet new building codes.

Finally, if you’ve done any recent remodeling, make sure your insurance reflects the increased value of your home.

Remember that a standard policy does not pay for damage caused by a flood or earthquake. Special coverage is needed to protect against these incidents. Your insurance company can let you know if your area is flood or earthquake-prone. The cost of coverage depends on your home’s location and corresponding risk.

Replacing your valuables

If something happens to your home, chances are the things inside will be damaged or destroyed as well. Your coverage depends on the type of policy you have. A cost value policy pays the cost to replace your belongings minus depreciation. A replacement cost policy reimburses you for the cost to replace the item.

There are limits on the losses that can be claimed for expensive items, such as artwork, jewelry, and collectibles. You can get additional coverage for these types of items by purchasing supplemental premiums.

To determine if you have enough insurance, you need to have a good handle on the value of your personal items. Create a detailed home inventory file that keeps track of the items in your home and the cost to replace them.

Create a home inventory file

It takes time to inventory your possessions, but it’s time well spent. The little bit of extra preparation can also keep your mind at ease. The best method for creating a home inventory list is to go through each room of your home and individually record the items of significant value. Simple inventory lists are available online. You can also sweep through each room with a video or digital camera and document each of your belongings. Your home inventory file should include the following items:

· Item description and quantity

· Manufacturer or brand name

· Serial number or model number

· Where the item was purchased

· Receipt or other proof of purchase / Photocopies of any appraisals, along with the name and address of the appraiser

· Date of purchase (or age)

· Current value

· Replacement cost

Pay special attention to highly valuable items such as electronics, artwork, jewelry, and collectibles.

Storing your home inventory list

Make sure your inventory list and images will be safe in case your home is damaged or destroyed. Store them in a safe deposit box, at the home of a friend or relative, or on an online Web storage site. Some insurance companies provide online storage for digital files. (Storing them on your home computer does you no good if your computer is stolen or damaged). Once you have an inventory file set up, be sure to update it as you make new purchases.

We invest a lot in our homes, so it’s important we take the necessary measures to safeguard it against financial and emotional loss in the wake of a disaster. Homeowners insurance is that safeguard, be sure you’re properly covered.

Q2 Western Washington Real Estate Market Update

The following analysis of the Western Washington real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please contact me!

ECONOMIC OVERVIEW

Washington State employment jumped back up to an annual growth rate of 2.4% following a disappointing slowdown earlier in the spring. As stated in the first quarter Gardner Report, the dismal numbers earlier this year were a function of the state re-benchmarking its data (which they do annually).

The state unemployment rate was 4.7%, marginally up from 4.5% a year ago. My current economic forecast suggests that statewide job growth in 2019 will rise by 2.6%, with a total of 87,500 new jobs created.

HOME SALES

- There were 22,281 home sales during the second quarter of 2019, representing a drop of 4.8% from the same period in 2018. On a more positive note, sales jumped 67.6% compared to the first quarter of this year.

- Since the middle of last year, there has been a rapid rise in the number of homes for sale, which is likely the reason sales have slowed. More choice means buyers can be more selective and take their time when choosing a home to buy.

- Compared to the second quarter of 2018, there were fewer sales in all counties except Whatcom and Lewis. The greatest declines were in Clallam, San Juan, and Jefferson counties.

- Listings rose 19% compared to the second quarter of 2018, but there are still a number of very tight markets where inventory levels are lower than a year ago. Generally, these are the smaller — and more affordable — markets, which suggests that affordability remains an issue.

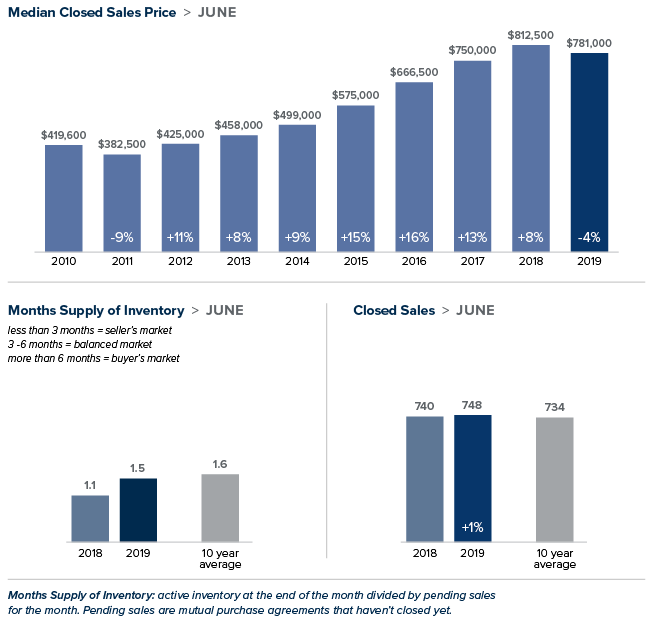

HOME PRICES

- Year-over-year price growth in Western Washington continues to taper. The average home price during second quarter was $540,781, which is 2.8% higher than a year ago. When compared to first quarter of this year, prices were up 12%.

- Home prices were higher in every county except King, which is unsurprising given the cost of homes in that area. Even though King County is home to the majority of jobs in the region, housing is out of reach for many and I anticipate that this will continue to act as a drag on price growth.

- When compared to the same period a year ago, price growth was strongest in Lewis County, where home prices were up 15.9%. Double-digit price increases were also seen in Mason, Cowlitz, Grays Harbor, and Skagit counties.

- The region’s economy remains robust, which should be a positive influence on price growth. That said, affordability issues are pervasive and will act as a headwind through the balance of the year, especially in those markets that are close to job centers. This will likely force some buyers to look further afield when searching for a new home.

DAYS ON MARKET

- The average number of days it took to sell a home matched the second quarter of 2018.

- Snohomish County was the tightest market in Western Washington, with homes taking an average of only 21 days to sell. There were five counties where the length of time it took to sell a home dropped compared to the same period a year ago. Market time rose in eight counties and two were unchanged.

- Across the entire region, it took an average of 41 days to sell a home in the second quarter of 2019. This was the same as a year ago but is down 20 days compared to the first quarter of 2019.

- As stated above, days-on-market dropped as we moved through the spring, but all markets are not equal. I suggest that this is not too much of an issue and that well-priced homes will continue to attract attention and sell fairly rapidly.

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors. I am leaving the needle in the same position as the first quarter as demand appears to still be strong.

The market has benefitted from a fairly significant drop in mortgage rates. With average 30-year fixed rates still below 4%, I expect buyers who have been sitting on the fence will become more active, especially given that they have more homes to choose from.

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

LOCAL MARKET UPDATE – JULY 2019

The market in our region appears to be moderating. Inventory is up, prices are relatively stable and homes are taking a bit longer to sell. However, with less than two months of available inventory, supply is still far short of demand. Steady buyer activity, low interest rates and a thriving economy are making for a strong summer in the housing market.

Seattle

>>>Click image to view full report.

Your Queen Anne Market Report for July 2019

What I suggested might happen to our market in last month’s report, namely that increased inventory would probably lead to a slow down to the market, has come to pass. In addition, we are now in the summer market which is usually slightly slower.

Having said that, homes are still appreciating quite well as demand for Queen Anne remains high due to its location and continuing low interest rates. The Fed is expected to cut the rate they charge banks next month and that usually leads to slightly lower mortgage rates so I see rates as continuing to be positive.

To recap the last 30 days, there have been 43 homes sell or close since my last report on June 10th. Seven of those have sold for more than full price. Of those 43 sold or pending homes, 10 were listed since June 10th. We currently have 44 active listings for sale which is about the same number as last month. Incidentally, I am seeing a less frantic pace of homes coming onto the market since the last report. This spring was truly something of a record breaker in terms of homes coming on the market. In the last 30 days, we have only had 18 homes listed for sale which is far less than the number listed in March, April and especially May. I expect this slower pace of homes being listed to continue through summer.

Many of you probably know that the WS Legislature has increased the excise rates you pay when your home sells. Please review this document which will let you know how much more it will cost you to sell your home beginning in January. FYI, the rate more than doubles for homes sold for $1.5M or more. Yikes!

The winner of last month’s home that sold for the most over its list price was 3338 9th West, listed for $1.195M and selling for $1.321M. After I previewed this home, I thought it was too low on the price, but the market gave us the current value. Please review this document for details of those homes that sold in the last 30 days.

And that’s the way Steve sees it…

Have fun outside if it ever stops raining! (At least it’s warmer).

Are You Better Off Paying Your Mortgage Earlier or Investing Your Money?

Photo Credit: Rawpixel via Unsplash

Few topics cause more division among economists than the age-old debate of whether you’re better off paying off your mortgage earlier, or investing that money instead. And there’s a good reason why that debate continues; both sides make compelling arguments.

For many people, their mortgage is the largest expense they will ever incur in their lives. So if given the chance, it only makes logical sense you would want to pay it off as quickly as possible. On the other hand, a mortgage is also the cheapest money you will ever borrow, and it’s generally considered good debt. Any extra money you obtain could be definitely be put to good use elsewhere.

The reality is, however, a little less cut and clear. For some homeowners, paying off their mortgage earlier is the right answer. While for others, it would be far more advantageous to invest their money.

Advantages of paying off your mortgage earlier

- You’ll pay less interest: Each time you make a mortgage payment, a portion is dedicated towards interest, and another towards principal (we’ll ignore other costs for now). Interest is calculated monthly by taking your remaining balance, the length of your amortization period, and the interest rate agreed upon with your lending institution.

If you have a $300,000 mortgage, at a 4% fixed rate over 30 years, your monthly payment would be around $1,432.25. By the time you finish paying off your mortgage, you would have paid a total of $515,609, of which $215,609 were interest.

If you wanted to lower the total amount you pay on interest, you don’t need to make a large lump sum to make a difference. If you were to increase your monthly mortgage payment to $1,632.25 (a $200 a month increase), you would be saving $50,298 in interest, and you’ll pay off your mortgage 6 years and 3 months earlier.

Though this is an oversimplified example, it shows how even a small increase in monthly payments makes a big difference in the long run.

- Every additional dollar towards your principal has a guaranteed return on investment: Every additional payment you make towards your mortgage has a direct effect in lowering the amount you pay in interest. In fact, each additional payment is, in fact, an investment. And unlike stocks, bonds, and other investment vehicles, you are guaranteed to have a return on your investment.

- Enforced discipline: It takes real commitment to invest your money wisely each month instead of spending it elsewhere.

Your monthly mortgage payments are a form of enforced discipline since you know you can’t afford to miss them. It’s far easier to set a higher monthly payment towards your mortgage and stick to it than making regular investments on your own.

Besides, once your home is completely paid off, you can dedicate a larger portion of your income towards investments, your children or grandchildren’s education, or simply cut down on your working hours.

Advantages of investing your money

- A greater return on your investment: The biggest reason why you should invest your money instead comes down to a simple, green truth: there’s more money to be made in investments.

Suppose that instead of dedicating an additional $200 towards your monthly mortgage payment, you decide to invest it in a conservative index fund which tracks S&P 500’s index. You start your investment today with $200 and add an additional $200 each month for the next 30 years. By the end of the term, if the index fund had a modest yield of 5% per year, you will have earned $91,739 in interest, and the total value of your investment would be $163,939.

If you think that 5% per year is a little too optimistic, all we have to do is see the S&P 500 performance between December 2002 and December 2012, which averaged an annual yield of 7.10%.

- A greater level of diversification: Real estate has historically been one of the safest vehicles of investment available, but it’s still subject to market forces and changes in government policies. The forces that affect the stock and bonds markets are not always the same that affect real estate, because the former are subject to their issuer’s economic performance, while property values could change due to local events.

By putting your extra money towards investments, you are diversifying your investment portfolio and spreading out your risk. If you are relying exclusively on the value of your home, you are in essence putting all your eggs in one basket.

- Greater liquidity: Homes are a great investment, but it takes time to sell a home even in the best of circumstances. So if you need emergency funds now, it’s a lot easier to sell stocks and bonds than a home.

Mortgage Rate Forecast

Geopolitical uncertainty is causing mortgage rates to drop. Windermere Chief Economist, Matthew Gardner, explains why this is and what you can expect to see mortgage rates do in the coming year.

Over the past few months we’ve seen a fairly significant drop in mortgage rates that has been essentially driven by geopolitical uncertainty – mainly caused by the trade war with China and ongoing discussions over tariffs with Mexico.

Now, mortgage rates are based on yields on 10-Year treasuries, and the interest rate on bonds tends to drop during times of economic uncertainty. When this occurs, mortgage rates also drop.

My current forecast model predicts that average 30-year mortgage rates will end 2019 at around 4.4%, and by the end of 2020 I expect to see the average 30-year rate just modestly higher at 4.6%.

To Buy New or Old, That is the Question

We are often asked, “Which is the better buy, a newer or older home?” Our answer: It all depends on your needs and personal preferences. We decided to put together a list of the six biggest differences between newer and older homes:

The neighborhood

Surprisingly, one of the biggest factors in choosing a new home isn’t the property itself, but rather the surrounding neighborhood. While new homes occasionally spring up in established communities, most are built in new developments. The settings are quite different, each with their own unique benefits.

Older neighborhoods often feature tree-lined streets; larger property lots; a wide array of architectural styles; easy walking access to mass transportation, restaurants and local shops; and more established relationships among neighbors.

New developments are better known for wider streets and quiet cul-de-sacs; controlled development; fewer aboveground utilities; more parks; and often newer public facilities (schools, libraries, pools, etc.). There are typically more children in newer communities, as well.

Consider your daily work commute, too. While not always true, older neighborhoods tend to be closer to major employment centers, mass transportation and multiple car routes (neighborhood arterials, highways and freeways).

Design and layout

If you like Victorian, Craftsman or Cape Cod style homes, it used to be that you would have to buy an older home from the appropriate era. But with new-home builders now offering modern takes on those classic designs, that’s no longer the case. There are even modern log homes available.

Have you given much thought to your floor plans? If you have your heart set on a family room, an entertainment kitchen, a home office and walk-in closets, you’ll likely want to buy a newer home—or plan to do some heavy remodeling of an older home. Unless they’ve already been remodeled, most older homes feature more basic layouts.

If you have a specific home-décor style in mind, you’ll want to take that into consideration, as well. Professional designers say it’s best if the style and era of your furnishings match the style and era of your house. But if you are willing to adapt, then the options are wide open.

Materials and craftsmanship

Homes built before material and labor costs spiked in the late 1950s have a reputation for higher-grade lumber and old-world craftsmanship (hardwood floors, old-growth timber supports, ornate siding, artistic molding, etc.).

However, newer homes have the benefit of modern materials and more advanced building codes (copper or polyurethane plumbing, better insulation, double-pane windows, modern electrical wiring, earthquake/ windstorm supports, etc.).

Current condition

The condition of a home for sale is always a top consideration for any buyer. However, age is a factor here, as well. For example, if the exterior of a newer home needs repainting, it’s a relatively easy task to determine the cost. But if it’s a home built before the 1970s, you have to also consider the fact that the underlying paint is most likely lead0based, and that the wood siding may have rot or other structural issues that need to be addressed before it can be recoated.

On the flip side, the mechanicals in older homes (lights, heating systems, sump pump, etc.) tend to be better built and last longer.

Outdoor space

One of the great things about older homes is that they usually come with mature tress and bushes already in place. Buyers of new homes may have to wait years for ornamental trees, fruit trees, roses, ferns, cacti and other long-term vegetation to fill in a yard, create shade, provide privacy, and develop into an inviting outdoor space. However, maybe you’re one of the many homeowners who prefer the wide-open, low-maintenance benefits of a lightly planted yard.

Car considerations

Like it or not, most of us are extremely dependent on our cars for daily transportation. And here again, you’ll find a big difference between newer and older homes. Newer homes almost always feature ample off-street parking: usually a two-care garage and a wide driveway. An older home, depending on just how old it is, may not offer a garage—and if it does, there’s often only enough space for one car. For people who don’t feel comfortable leaving their car on the street, this alone can be a determining factor.

Finalizing your decision

While the differences between older and newer homes are striking, there’s certainly no right or wrong answer. It is a matter of personal taste, and what is available in your desired area. To quickly determine which direction your taste trends, use the information above to make a list of your most desired features, then categorize those according to the type of house in which they’re most likely to be found. The results can often be telling.

If you have questions about newer versus older homes, I can help you, let’s talk!

The Housing Market in 2019

The last time we saw a balanced market was late 1990s, meaning many sellers and buyers have never seen a normal housing market. Windermere Real Estate’s Chief Economist Matthew Gardner looks at more longer-term averages, what does he see for the future of the housing market?

Windermere Supports Red Nose Day

Originating in the U.K. in 1988, Red Nose Day started to help end child poverty. In 2015, the public charity, Comic Relief USA, launched the campaign in the U.S.

Last year, the Red Nose campaign raised $47 million, setting the total raised since 2015 to over $150 million, and have changed the lives of over 16 million children. These funds help buy vaccines and medical services, as well as meals, educational assistance and more. Half of the money raised supports programs in the 50 states and Puerto Rico, and the other half helps fund programs in Latin America, Africa, and Asia.

Companies like Bill and Melinda Gates Foundation, M&M’s, Mars Wrigley Confectionary, and NBC have supported the organization as national and programming partners. NBC will have a celebrity-filled Red Nose Day program planned at 8/7 c tonight.

We’ve supported Red Nose Day for the last two years through our philanthropic arm, Windermere Foundation, this year we were happy to give $1000, not to mention the red noses! We are proud to help organizations in our local and global communities who work to support low-income and homeless families. Please join us again this year in giving to this important campaign to end child poverty.

To participate, you can get your $2 Red Nose at your nearest Walgreens. Of that, $1.30 goes to the fund. The nose purchase is not tax deductible, but a donation made directly to them is. You can donate online at https://donation.rednoseday.org/.

To learn more about the organization and who they help, and how you can participate, go to their website: https://rednoseday.org/home.